Forty ways to pay for coffee in Japan

Patrick McKenzie (patio11) reads his 2021 essay "Payments in Japan," tracing how Japanese consumers navigate a landscape with dozens of competing payment methods at once: credit cards, electronic money, QR-code super apps, convenience-store cash vouchers, and bank transfers. Along the way he covers the JFTC's campaign to force credit card networks to disclose interchange rates, how Rakuten and 7-Eleven each bought a bank to solve a payments problem blocking their core business, why PayPay's subsidized 2018 launch let it run away with the QR code market, and why konbini payments remain popular despite a user experience frozen in the late 1990s.

Presenting Sponsors: Mercury & MongoDB

Complex Systems' presenting sponsor is Mercury: radically better banking for founders. Mercury's new feature Command brings an LLM directly into your banking interface, so checking balances, finding invoices, or sending a wire is as easy as asking. Apply online in minutes at https://mercury.com/.

What's the point of building faster with AI if your database can't keep up? MongoDB's native data model mirrors the language LLMs already speak. Ship at the speed of AI while staying ACID compliant at Fortune 500 scale. Start building at https://mongodb.com/ai.

Timestamps:

(00:00) Intro

(02:44) Credit cards

(10:40) Payment method heterogeneity

(12:57) Cash

(14:57) Sponsors: Mercury + MongoDB

(17:29) Cash (cont’d)

(19:58) Electronic money systems

(22:13) App-based payments

(28:27) Convenience store payments

(31:27) Bank transfers

(34:03) Ambitions thwarted

(34:30) Wrap

Transcript

Welcome to Complex Systems, where we discuss the technical, organizational, and human factors underpinning why the world works the way it does.

Hideho, everybody. My name is Patrick McKenzie, better known as patio11 on the internet. I'm recording this episode from Chicago shortly before my family's annual trip to Japan, where I previously lived for about twenty years, and I'm looking at an essay that I wrote back in 2021 called “Payments in Japan.”

This is a topic of somewhat narrow, specialized interest compared to many things that we discuss on this podcast, but it's intellectually interesting to me. I think payments in other countries helps provide a bit of a lens on how we approach payments in, for example, the United States or Europe, and some of the claims in this essay have aged in a manner that I feel like patting myself on the back.

So I thought I would do a read of the essay, interspersed with some live commentary on what has changed since it was originally written. And with that, the essay, “Payments in Japan,” originally published in Bits About Money on November 19th, 2021.

One of the advantages of living (spiritually, if not physically) in two countries is you get to see the future arriving early, in both directions. In the almost twenty years I’ve lived in Japan, the linguistic and geographic barriers to understanding daily life here have lessened (a topic worth an essay in itself), but they are still formidable. This makes an international mindset a surprisingly durable source of alpha, even in professional fields, even ones which are intensely globalized.

As an aside, 2021 is before LLMs reinvented the world. I do wonder whether LLMs won't, quite durably, decrease the amount of wall of competence that's required, linguistically, to do trade in ideas between nations. But, neither here nor there.

Take money, for example. I have a literal degree in East Asian Studies, and while money was implicated (economy, business, work culture, etc.) and I was taught how to count it, the culture that is money came up precisely once: “Japan is a cash-based society.”

If you read the same textbook, or if you’ve read no textbook at all, here are some updates to the state of the world:

Payments in Japan have changed enormously in the last 20 years. The rate of change is accelerating. You will see some echoes of some of these trends where you live, sooner rather than later.

I have to reiterate my usual disclaimer: I work at Stripe, but the following are my own opinions. Also, you can reasonably assume that I'm personally or professionally exposed to almost every company in the Japanese payments space; in addition to it being my literal job to keep on top of it, I also find it convenient to e.g. be able to buy coffee.

And, as an aside: of course, I no longer work full-time at Stripe, but I'm still an advisor there, and they still do not necessarily endorse things that I say in my personal spaces.

Credit cards

The overall business of credit cards and debit cards is similar in Japan to the United States. Feel free to read those essays if you need a refresher on the overall model.

There are some differences in underlying infrastructure (e.g. Japan has a national switch — CAFIS — sitting in the middle of several global payment rails) that would only interest payment geeks. More interesting are some changes in the fundamental UX of cards.

In Japan, credit cards are payment instruments first and loan originators a long second. You have to opt-in to the provision of credit and announce your intention to do so to the store clerk.

For Japanese readers: in the United States, when you get your statement, you can pay in full, in which case you will not be charged interest, or you can pay any amount less than full but more than a specified minimum payment, in which case you will be charged interest on a revolving basis, starting on the day you made the transaction but being assessed in the statement cycle following the one you didn’t pay in full.

You are correct, this system is virtually incomprehensible to people not professionally involved in it, and it is a cause of much angst for users and regulators of the financial industry. It is probably because of America's inscrutable culture.

(Since arch humor does not always travel well, I'll make that explicit: Japan is widely considered, both domestically and abroad, to have a culture which is somehow extremely distinctive and explains almost any imaginable difference between Japan and the rest of the world. The story is much more complicated than is popularly believed. If you only read one book about it, Sugimoto's Introduction to Japanese Society may be among the best available.)

Anyhow, back to payments, because understanding payments’ material reality is much more useful to predict the world than reasoning from first principles about capital-C Culture.

The intense friction associated with accessing credit makes spending on credit far, far less common than in other nations. Of course, and contrary to the belief of many, Japanese consumers do actually use credit and are sometimes unhappy when they cannot use it, such as when checkout systems don’t offer the option to “split the payment” (pay in a fixed number of installments with an equivalent-to-interest fee charged later by the card issuer) or “pay it with revolving [credit].” This is often forgotten in discussions of localizing globally-produced services for the market. Money is a culture all to itself!

Quite a bit of the UX of Japanese credit card apps is around managing the (extremely ponderous and legacy-heavy) mechanics of recategorizing previous payments from single-payment to split-payment to revolving credit and back again.

Interchange rates in Japan are not materially regulated, relatively high, and treated as commercial secrets. They’re on a need-to-know basis and the industry feels you don’t need to know, even if you (...hypothetically) process credit card payments. The Japanese Fair Trade Commission has taken a dim view of this publicly and is investigating the matter.

And an update, more than five years later: they continued to take a very dim view of it publicly, and I'll read you some updates since 2021. On April 8th, 2022, the JFTC published its market survey report on credit card transactions and found that none of the standard interchange fee rates were disclosed in Japan, versus sixty-plus countries in which at least one brand disclosed those rates.

There was a cabinet decision on June 7th, 2022, titled “A New Form of Capitalism,” which called for disclosure, noting that interchange accounts for roughly 70% of merchant fees. Then the JFTC and METI jointly announced a policy in September 2022 that Mastercard, UnionPay, and Visa would release their standard rate schedules. And indeed, they went on to release their standard rate schedules.

Now, their standard rate schedules are still pretty high relative to the United States, which doesn't materially cap credit card interchange, and quite high relative to the way the EU caps it at 0.2% to 0.3%, and how the Durbin Amendment, for example, in the United States caps debit card payments. But the secrecy thing has indeed been essentially repealed.

There was also a raid on a large global credit card brand in 2024, conducted by the Japanese Fair Trade Commission, and you can read more about that in other spaces. The credit card brand has subsequently settled with the JFTC over the matter.

Okay, back to the essay.

The same applies to debit as well as credit, which means that Japanese debit cards often earn rewards at the same rate as credit cards (never a basis point more than 1%, a curious bit of pricing discipline which I will not further comment about explicitly).

Rereading that five years later — yeah, that is the salaryman winking directly at the camera. There are, strictly speaking, some cards in Japan that pay slightly more than 1%, and quite less than prevailing interchange rates. Interested listeners may ask an LLM of choice.

No discussion about credit cards in Japan would be complete without mentioning JCB, which has about 20% of the market — or at least did back in 2021.

Credit cards are the original network effects business. Big networks eat smaller networks alive. Most countries did not have the complex mix of factors decades ago, when credit card networks were incubating, to support domestic networks which achieved escape velocity from the global payments networks.

Japan did, and JCB is the result. It is likely China will also have enduring domestic / domestic++ credit card networks (UnionPay, etc.); it feels far less likely that many other nations will develop them in the future. One interesting question for the payments industry is whether new payment methods will see global consolidation (as credit card networks did), have regional winners, or have national++ networks.

My personal prediction is “You’ll actually see all three,” driven by a mix of regulatory desires worldwide to move more of their payments business “closer to home” (and, sometimes, to avoid explicitly American control of non-American financial rails), flourishing customer choice in using different payment methods for different use cases and those use cases naturally being more or less geographically-bounded (international travel versus subway rides, for example), savvy bizdev teams, technology substrates like e.g. mobile platform penetration, and other factors.

One other fun note about credit cards in Japan: in the U.S., tech companies are often seen as muscling in on the financial industry’s turf. In Japan, tech companies are a growth engine for the financial industry. Rakuten Card is either the largest or second largest issuer in Japan, and it exists because Rakuten’s core business, an eBay-meets-Shopify marketplace, suffered majorly from many customers having no trusted way to pay online in the late 1990s.

So they did the natural thing for a tech firm. They bought a bank and onboarded tens of millions of Japanese users to credit cards for the first time ever. It seemed neater. (This is a callback to Ken Watanabe's character's line in the movie Inception, where he just buys an airline because it's necessary for a plot point.)

Jokes aside, Rakuten embraced early something that many ecosystems will in the coming years: payments makes existing franchises stronger. Their core loop is getting someone onto their payment rails as a convenience to use the core business, capturing their payments business outside of their own ecosystem (which is margin accretive), rewarding their users with points for that business, and making those points most useful within their own ecosystem than they are outside of it. This brings the users back and encourages them to move more of their business to Rakuten’s (many, many) product lines versus their competitors.

This isn’t dissimilar to the reason why every bank wants payment rails: it keeps you with the bank, earns the bank revenue even when you’re not transacting directly with the bank, and will bring you back to the bank’s product lines in the future.

Increasingly, the same logic will apply to non-bank firms which have broad user bases. It may even eventually apply to large user bases centralized around something which is not traditionally described as a firm. (A potentially interesting fintech interview question: “What is the smallest number of things that would have to change about the world for Beyoncé to offer a credit card?”)

This will drive what I believe is a defining feature of the future of payments:

Payment method heterogeneity

If you go to a grocery store in the United States, you have functionally four payment choices: cards, checks, cash, and (often forgotten by technologists, for predictable reasons) publicly-provided benefits.

When I bought my morning coffee at the friendly neighborhood 7-Eleven convenience store today, I asked the shop staff for permission to take a few photos. They illustrate a trend that I would bet on hitting most of the world: payment method heterogeneity. In Japan, we are witnessing a Cambrian explosion in payment providers, payment systems, and payment modalities.

A picture worth a thousand words:

Here's a picture which is worth a thousand words, and you can see it in the show notes, but I'll narrate out loud the salient bits to you. The top of the picture says, “Goriyō kan no o-shiharai hōhō,” which just means “payment methods that you can use at this store.” It has essentially four quadrants to it. We've got electronic money in the top left, with approximately eleven brands represented. We have credit cards in the top right, which has all the usual brands you'd expect, plus some that a listener to this podcast has presumptively never heard of. In the bottom left, we have barcode payments, which shows more than twelve brands, led by PayPay, which we're going to discuss in a moment. And then in the bottom right, it has mobile payments, including the logo for Apple Pay, Google Pay, and then something you're unlikely to have heard of, the Quo Card.

That is 40 payment brands (though not 40 distinct rails) all vying for customers, retailers, mindshare, share of wallet, and customer habits. And that isn’t nearly all of them.

You almost certainly recognize some of these logos, particularly in the top right (credit card networks) and the bottom right (mobile payments wallets by Apple and Google).

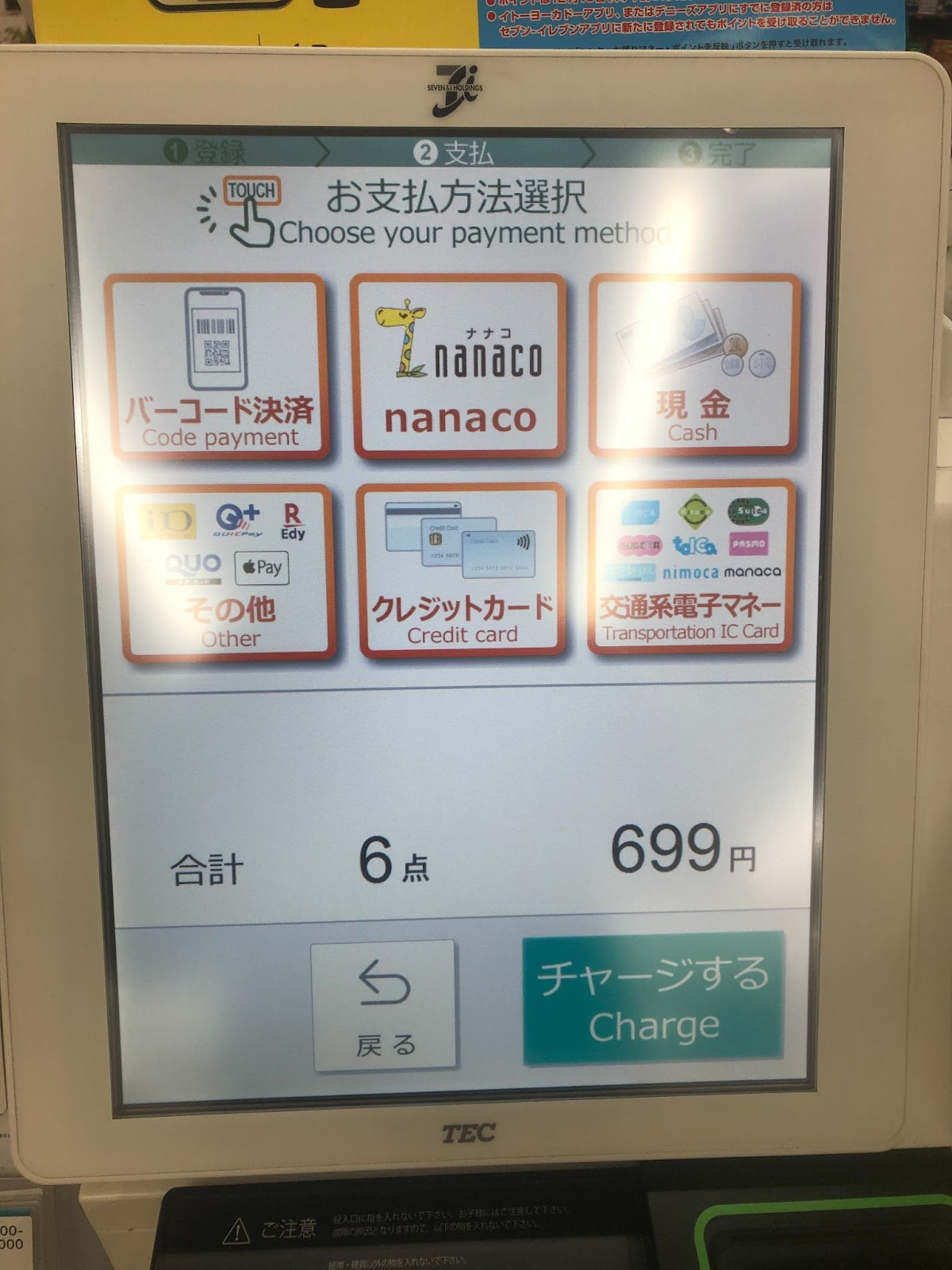

Here is the same question asked at point-of-sale. (Apologies for the poor-quality photo; I was attempting to not impose upon my friendly neighborhood clerks and optimized for speed over quality.)

And apologies for the poor quality of this photo — although podcast listeners presumably don't care about that too much — but it's also in the show notes. So the screen asks, in both Japanese and English, for the benefit of the many foreign tourists who use 7-Eleven, “Choose your payment method,” and it gives you six options: a barcode payment; Nanaco, which is 7-Eleven's domestic payment rail; cash; “other,” which lists Apple Pay among a few other things you're less likely to have heard of; credit cards; and then transportation IC cards.

Let’s take them somewhat out of order, for reasons which will become apparent later:

Cash

What is there to say about cash? Volumes worth, nothing at all, or something in between. Since a newsletter or a podcast isn’t a place for a historical treatis e, I’ll make one casual observation and one serious one.

The casual observation: An older gentleman in front of me in line (back in 2021) asked how to pay cash for a purchase at this store. I was surprised, and then I was surprised that I was surprised, that anyone at a convenience store in central Tokyo would still use cash. That might have been the first cash transaction I observed in this store during the pandemic.

The pandemic has accelerated many existing trends worldwide, and it certainly provided a boost to the financial industry and government’s long, mutual plan to transition Japan to less dependence on cash for routine transactions.

The financial industry wants this because money. In a low-interest environment, which has described Japan for 30 years and counting, payments are (by far) the most lucrative product to sell to most customers.

The government wants this for more complicated reasons. Some are predictable from Seeing Like a State; governments prefer legible things to illegible things like humans prefer oxygen to carbon monoxide. Digital payments are more legible than cash. No conspiracy is required; governments will, given the ability, organize their environments to have more digital payments and less cash and cash-like payments, often without even needing to intend this.

In Japan though, this is definitely an explicit, declared plan. Japan wants to increase digital payments’ share to 40%, up from about 20% currently. Some of the proffered reasons are decreasing the tax gap (which, perhaps surprisingly to external observers, Japan is institutionally convinced is rather high) and supporting the financial industry. As I've mentioned previously, the financial industry everywhere is considered systemically important is a privately-owned publicly-relevant policy arm.

I will make an aside here: we often have this background belief that government cannot possibly achieve its goals. Japan did achieve the 40% target one year ahead of schedule, and has new targets over the course of the coming years. Let me quickly look them up.

So the new goals are 65% by 2030, and 80% long-term.

One experiment Japan rolled out in the last year or so was My Number Points. My Number is a recent (and sometimes controversial) national identification scheme, giving a large number of nationally- and locally-administered government services a single identification number for every resident of Japan.

One claimed benefit of the system is that it will be easier to administer stimulus directly with it. My Number Points were a trial run at this. The government offered 25% cash back, administered via your preferred payments provider, if you opted into it with that payment provider, demonstrated you were uniquely getting the benefit for yourself that one time by providing your My Number card, and went through a (paaaaaainful) UX.

The benefit was capped at 5,000 yen a person (about $50) — actually substantially less these days, but many people would round it to $50 anyway, even though it's closer to $30 now — and probably did not cause a sea change in customer attitudes about payment methods.

A more effective intervention was on the other side of the market: Japan had a variety of subsidies to encourage uptake of “cashless” payments systems on the business side of the market, reasoning that making electronic payments systemically more convenient would encourage more user adoption of them, which would drag along holdouts, which would encourage more user adoption, etc.

One such campaign, recently sunset ( as of 2021) but still mentioned by many vendors as of this writing ( again back in 2021) (e.g. see Rakuten Pay's solicitation, if you can read Japanese), was that the government would subsidize half of the cost of terminals (up to about $300) if a) payments providers were willing to cover the other half and b) payments providers temporarily zeroed out the cost of interchange (and other fees) through October 2021. The government offered to subsidize the cost of the interchange as well.

As you can imagine, businesses often respond positively to the government offering them free money, and the payments industry used its very large boots-on-the-ground sales force to move many, many, many POS systems into eateries, cafes, small apparel shops, and other businesses in Japan where penetration of credit card readers had historically lagged.

This was accidentally accelerated by the coronavirus epidemic. Shops were looking for ways to improve their physical environment and market those improvements as being health-protecting, to bring foot traffic back, and “No need to touch the staff’s hands even indirectly” suddenly became a very popular selling point.

The first widespread entry in contactless payments is almost 20 years old:

Electronic money systems

The original entry into contactless payments in Japan, available since the early 2000s (after a rich history [PDF] of transportation-specific payment systems out of scope here), was so-called electronic money systems. The payments geek shorthand is “closed-loop stored value transportation cards which turned into open-loop stored value IC cards.” Got it? Good.

If you would prefer that explanation in more words:

Transportation systems worldwide have interesting payment problems. Japan has many interlinked transportation systems, owned by a variety of public and private entities, and strongly encourages intermodal transportation. This makes the payments problem even harder, and it is already hard enough in transport: the designed throughput of a turnstile at a Tokyo subway station is faster than credit cards can be sequentially authorized.

So the transportation companies developed systems with several goals, and speed, speed, speed was one of the dominant ones. This led to prepaid cards with a chip in them. Unlike credit cards, which are conceptually speaking a pointer to a record in a bank’s database about you, the prepaid cards contain the money “on the chip.” While there is eventually a recordkeeping process in a database (and the actual money is, of course, in the formal financial system and not on a card), the turnstile can verify funds availability (or charge you, on the way out) without needing to hit the network.

This makes it robust against outages (always a design consideration for infrastructure in Japan, to the credit of its engineering community) and optimizes for speed.

Transportation systems often have ancillary goods and services co-located with them, like e.g. cafes, convenience stores, flower shops, etc. As the Suica and other payments methods became so obviously superior to pre-buying tickets in advance, these shops started to say “Wouldn’t it be great if you could just tap the same card for a coffee? We are also acutely throughput constrained. We could also use a low-cost payments method is economically viable on extremely low ticket sizes.”

And, to simplify two decades of business development, the various operators figured out interoperability, you can use your Suica/Pasmo/etc. interchangeably for almost all ground-based transit, most ancillary services, and most convenience stores, and you can even put them in your phone these days.

Fun fact: your phone (very probably) sports a little extra silicon specifically to support this use case. Yes, your phone. It’s cheaper at global scales to put it in every phone versus having to support multiple supply chains and try to walk users through this product matrix.

Weirdly, penetration of the electronic money systems grew and then… stagnated. They’re functionally unusable online, despite some efforts to change that. The transit operators are not fundamentally payment businesses and have not executed well on improving merchant adoption after some (brilliant) work to get them accepted by large convenience store and cafe chains. Rakuten (Edy), 7/11 (Nanaco), and a few other large players all tried their own entries, and while many are sustainable businesses none caught fire.

And I will say, as an aside: they've continued to lose share in Japan in the last couple of years against app-based payments, which we'll discuss next.

The hot market in Japanese payments is:

App-based payments

QR codes have been big in Japan for almost 20 years, despite flopping so catastrophically in the U.S. that the CueCat is still a joke among technologists of a certain age. (Interestingly, that may have caused technologists to overlook how useful QR codes are.)

I will say, as an aside: I saw QR codes in many places in Silicon Valley on a recent trip there. I think the U.S. has largely caught up on QR code adoption as a useful technology, with standard iPhones and Androids. We've caught up to the utility of QR codes in the U.S. over the last five years. I did not necessarily see that one coming.

The core use case for QR codes in Japan used to be communicating URLs to users in physical space. Technologists who grew up reading English often don’t appreciate that https://URLなんて みやすいとは かぎりませんよ.com is how they read to many people in the world. Understandably, McDonald’s felt it was difficult to direct in-restaurant customers to URLs that felt like that to e.g. get menu information or download coupons, and so QR codes took off here. The UX of scanning them is ingrained in most phone users’ muscle memories.

Enter app-based payments, which largely (but not exclusively) use QR codes to bridge the gap between the user and store, in one of two ways:

The extremely easy to deploy way:

You see this extremely commonly in China and less in Japan, but it definitely exists (at e.g. my local sandwich shop): the store has one static QR code, printed near the register, with the logo of the supporting app near it. To pay, you scan the code in the app, key in the amount, and click Send. The store instantly receives notification of the payment on either a tablet that the payment scheme gave them or alternatively on a clerk’s cell phone.

The more common integrated method:

This requires that the store have a supported point-of-sale system, but is generally a better user experience.

Either a) the user initiates the transaction by showing a dynamically generated QR code from their phone to the clerk, who scans it or b) the store initiates the transaction by showing a dynamically generated QR code to the user, who scans it. The point-of-sales system does an online handshake with the payments scheme, syncing information about the transaction in progress (which the payments scheme is, notably, totally unaware of in the above deployment method). The user is immediately charged the amount they agreed to pay.

These are often referred to as QR-code payments but the payment apps are so-called “super apps,” and while payments is their dominant use case it is a tip of the iceberg. I prefer thinking of them as application ecosystems with a payments bit attached rather than as QR-codes with ancillary features.

The one that appears to be running away with the Japanese market, of many entries, is PayPay. To my discredit as a payments geek, I originally did not notice their entry into the market because mild dyslexia convinced me I already had an account, and so missed their primary user acquisition strategy in late 2018, which was paying people gobsmacking amounts of money just to sign up.

It is something of de rigeur in the U.S. tech community to laugh at Softbank for splashing large amounts of money to win large markets. PayPay, a joint venture between Softbank, Yahoo Japan, and Indian payments company Paytm (and isn’t that a sentence worth mentioning in discussions of globalization), spent hundreds of millions of dollars directly subsidizing user growth, which it achieved meteorically.

There are presumably videos you can watch of the UX on the Internet. The short version: it is really, really good. It may be the best Japan-specific software available on your phone. Not just in payments; it is the best software period. It is a fintech’s geek’s idealized dream of how good a core user experience can be. I could also list some quibbles, for example a KYC process which thinks I am not a person who could actually exist, but the core use is amazing.

I will say the core use case has aged a little bit. It is not quite as superior, relative to the rest of the market, as it was back in 2021, but it's still pretty good. It can also, interestingly, be used from outside of Japan, although PayPay does not make that widely known, and is useful for those people who have one part of their heart perpetually in the physical borders of Japan and a larger part of their body temporarily outside of it.

In addition to payments, it supports free instant transfers to friends (which are generally locked within the ecosystem), a points- and rank-based reward system, some bizdev tieups with the likes of Uber Eats and Yahoo Auctions (the eBay of Japan), ancillary financial services, a truly I-can’t-believe-thats-allowed system which will “simulate” “investment” of your points, etc.

If one were a PM at a payments app, whether PayPay, Line Pay, or e.g. Cash App in the U.S., one dominant concern might be “How do I minimize my users’ perceived need to install multiple of my competitors’ apps?” That’s a fun intuition pump and predicts some things that have actually already happened. One example might be two payment apps deciding to make mutually compatible QR codes (your users can read my codes, my users can read your codes, and this Just Works™) and settle between their respective financial ecosystems on the back-end, in return for soft agreements that they will not expand into each other’s turf directly.

By the way, in the five years since I wrote this essay, PayPay has continued to lock up the Japanese QR code market.

Convenience store payments

Convenience stores not only take payments, they have their own payment rails, because every ecosystem and every infrastructure player has a natural synergy with payment rails.

These still account for about 15% or so of Japanese e-commerce, and solve for a few different issues for an e-commerce user and business.

Problem: it’s tough to push cash through your computer screen and cash-on-delivery, offered pervasively by Japanese logistics firms, requires you to be home to accept the delivery.

Solution: the e-commerce site gives you a payment reference number and instructions, on an optionally printable voucher, to take to a designated convenience store chain. You go to any of their locations and pay in cash. The convenience store chain instantly tells the store that your payment was good and later settles with them electronically, mixing the actual physical cash with their giant flowing river of an operational problem. (Do you know what 7-Eleven did to solve this problem? Of course you do. They bought a bank so they can recycle the cash into on-premises ATMs without leaking tiny convenience store margins.)

Konbini payments (spelled after the most popular romanization for the shortened form of convenience store) are conceptually beautiful. The actual UX of them is pretty terrible, mostly because the integration layer (the actual surface a user sees) was coded in the late 1990s and hasn’t seen an update since, anywhere.

If you go to Amazon and try to pay with konbini payments today, (at least as of 2021, the last time I tried this,) you get to appreciate that late 90s orange chrome aesthetic one more time.

Why do users like konbini payments? They’re accessible: literally anyone can use them. Salaryman, child, and immigrant alike are equal in the eyes of the konbini system; it turns cash into HTTP requests for them all. They’re secure: many Japanese consumers were burned on credit cards with unauthorized or dubiously authorized recurring transactions from merchants, and while there are legal and structural protections against that, nothing has the peace of mind of “I will know, absolutely positively, that the only money I pay you will be cash I lay out on the counter.” They’re privacy preserving: sometimes people want to buy things without e.g. family members knowing about the transaction, and konbini payments are (while not anonymous) the easiest way to do that.

Convenience stores also have one complementary offering: they can take delivery of parcels for you, from e.g. Amazon, and hold them until you come by. This a nice example of infrastructure improving the world in a delightful way, and free to the user (konbinis love recurring foot traffic). A common use case is “I’m a salaryman and will not be home at any conveniently predictable hour to take delivery; the local konbini is open 24/7/365.”

A less common one, but one of the beautiful emergent things that happens once you get a new capability, is “I’m visiting my parents-in-law and would like to get them a gift but would like to hand it to them rather than having a delivery person do so, so I will ship it to the convenience store next door and unbox it myself rather than shipping it to them directly.”

Bank transfers

The dominant platform for B2B transfers in Japan is bank transfers (furikomi). To make this brief I’ll concentrate on the differences with ACH transfers in the U.S.: they’re functionally instant within banking hours, have finality guarantees closer to a wire transfer than an ACH payment, have a direct cost ($1 to $8 or so, depending on the sending bank’s pricing matrix, size of the transfer, and whether the sender is a consumer or business), and are reconciled manually a truly depressing portion of the time.

Reconciliation is matching your invoices (anticipated payments) with your bank statement (received payments). Furikomi have very limited metadata on them (customer name and phone number), and if you want to automate the matching, you need to instruct the customer to overwrite their name at their bank and include a reference number. Users will frequently botch this and so you will need to evaluate the instantaneous transfer later at human-powered speeds with a staff of overworked clerks looking at transaction amounts, timing, historical records, and similar to guess whether Taro Tanaka is paying on invoice #35234 issued to a company (“Maybe his employer?”) or invoice #234235 issued to Junichiro Tanaka (“Maybe a family member and not one of the several million people sharing that last name with no relation?”)

There was a similar system, PayEasy, developed which allowed business users to push transaction data to a financial intermediary prior to giving the user a reference number, so that transfers would deterministically resolve in real time. It enjoys quite a bit of adoption by governments for tax payments but comparatively little by the private sector.

Furikomi have benefited enormously from advances in online and mobile banking, which are (unfortunately) several years behind peer nations in their UXes. It no longer requires queuing for a teller or visiting an ATM to make one. That said, due to the reconciliation issue and UX issues, they lag in adoption for smaller ticket and B2C purchases.

This is often not appreciated: “Why are businesses happy to pay for payments?” One reason: if you enact high-friction walls around giving you money, people are less likely to give you money, and you would prefer the money even at a marginal cost to no money at all. That seems almost unmentionably straightforward and yet is underappreciated by many who model payments as “a tax” on sellers of goods and services. Another reason: you should prefer to have computers count money versus having people count money, because they are faster, cheaper, and less error prone, and that directly affects the UX you can offer users.

Ambitions thwarted

I had thought I could jot down most relevant things I knew about the Japanese payments market in time to make press, but ended up only making a tiny dent in the surface. Let me know if this sort of thing is interesting; if so, I’ll be happy to elaborate on Japan and perhaps cover other major markets in the future.

If you enjoy this topic, please come visit once it is safe to do so and give the payments ecosystem here a spin while enjoying Japan’s many, many reasons to visit. I would predict with high confidence you’ll see something that you will eventually see at home.

And indeed, since the pandemic, travel in Japan has taken off quite a bit. I think it's recovered onto the previous trend line, which is wonderful for the many tourists — at least to the extent that they don't see their tourist place of choice overcrowded. Somewhat less relevant for me, as I'm often mistaken for a tourist while being in Japan, but that's neither here nor there.

Anyway, thanks very much for listening to Complex Systems this week, and I will see you back again at the usual time next week, hopefully, and we'll soon be back in the usual studio. Have a good rest of your week.

Thanks for tuning in to this week's episode of Complex Systems. If you have comments, drop me an email or hit me up at patio11 on Twitter. Ratings and reviews are the lifeblood of new podcasts, for SEO reasons, and also because they let me know what you like.